Robustness Analysis

Robustness analysis inspired by Section 3.10, using the Growth+ model for internal validity and sensitivity experiments.

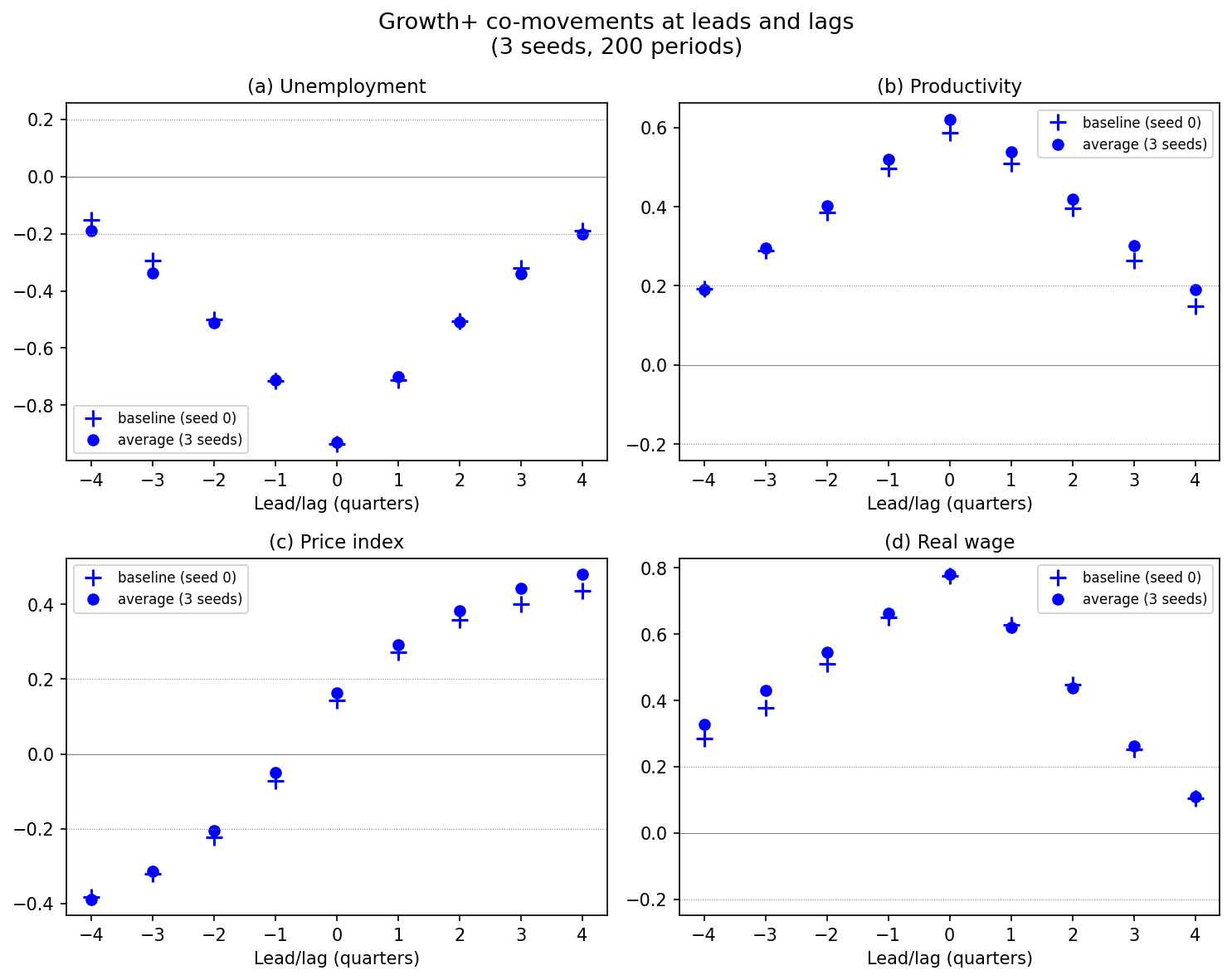

Internal validity: cross-correlations of unemployment, productivity, price index, and real wage with GDP across multiple seeds.

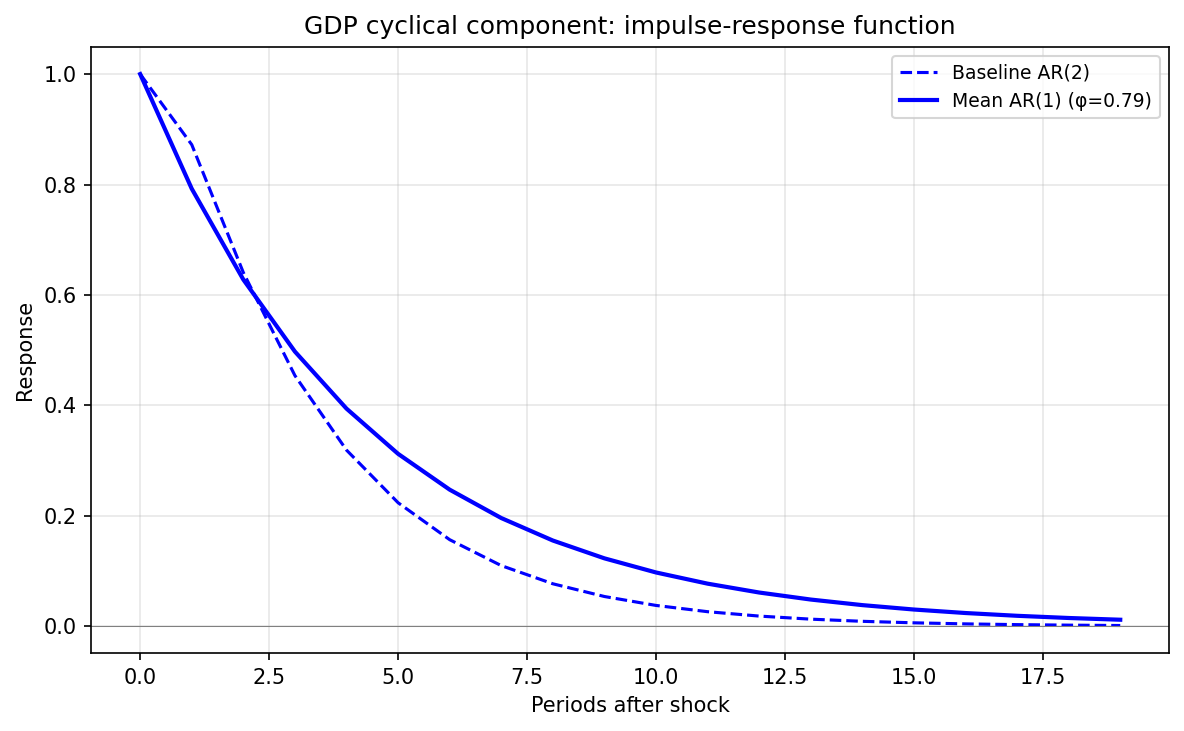

AR(2) vs AR(1) impulse-response functions for the GDP cyclical component.

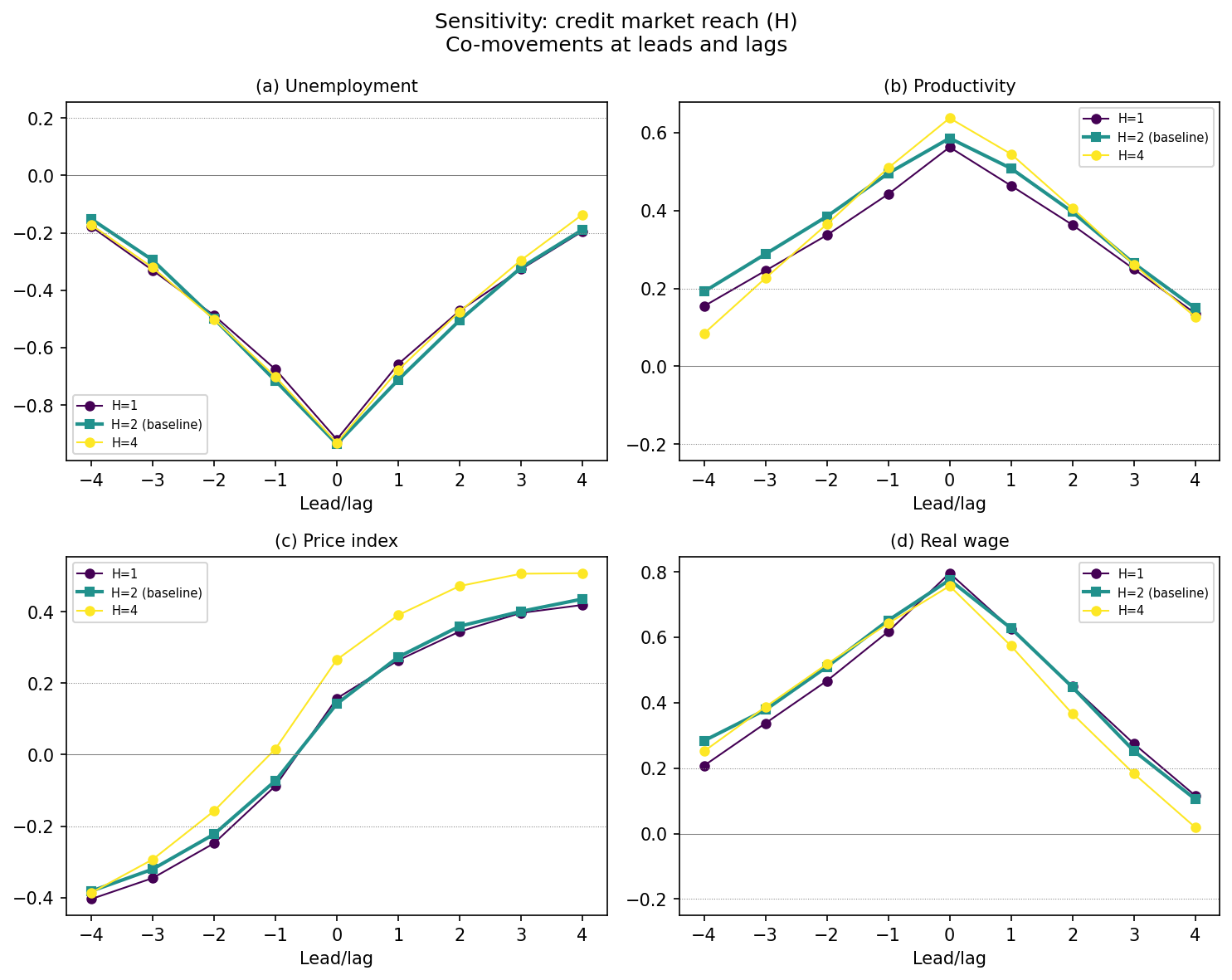

Sensitivity analysis: co-movement structure under different values of the credit market reach parameter H.

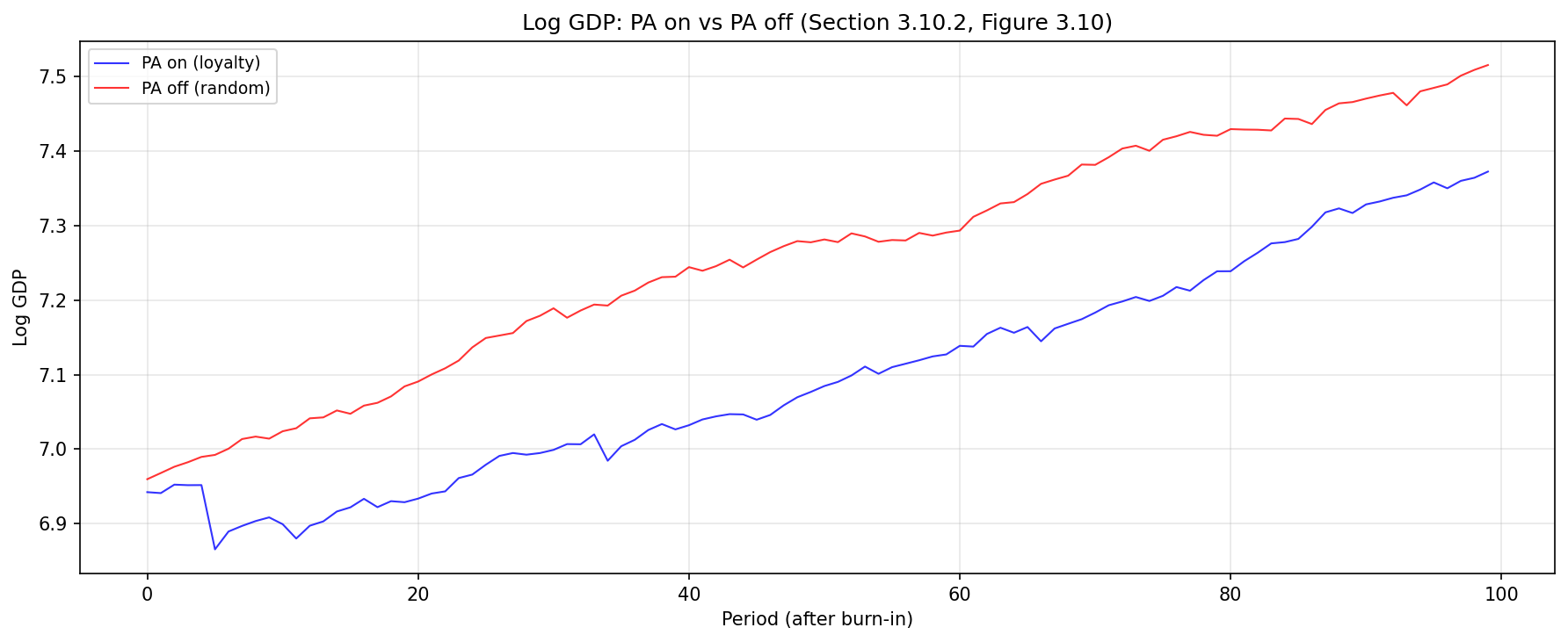

Structural experiment comparing log GDP under loyalty-based vs random consumer matching (Section 3.10.2, Figure 3.10).

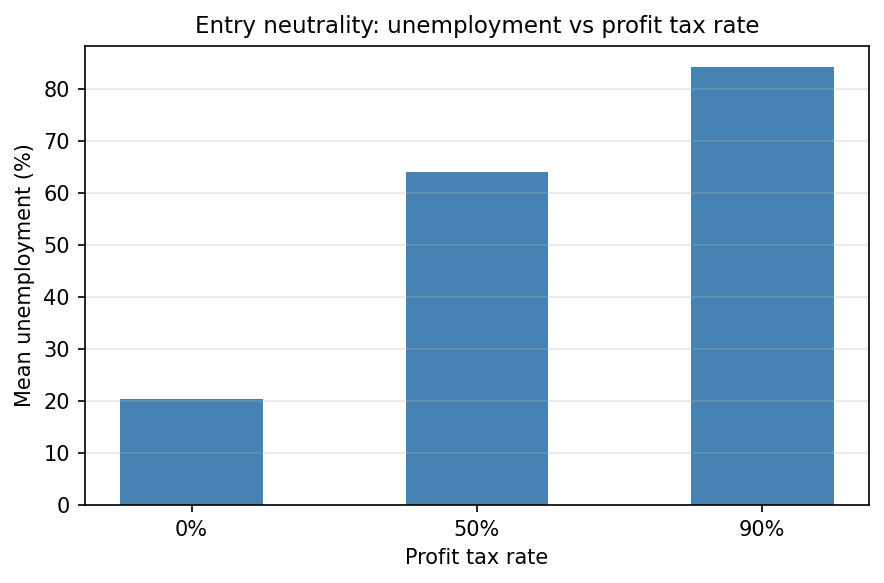

Entry neutrality: mean unemployment across three profit tax rate levels.

Run this yourself:

import bamengine as bam

from extensions.rnd import RND

sim = bam.Simulation.init(seed=42)

sim.use(RND)

results = sim.run(n_periods=1000, collect=True)See the full example.

On this page